Midyear Review: From Spring Slump to Summer Surge

Dimensional Fund Advisors

The US market struck fresh highs near the year’s midway point, rallying after taking a downward turn in March as investors weighed the impact of the war in Iran, among other factors. Driven by chipmakers and other technology stocks, the S&P 500 Index hit record levels in late May and early June followed by up-and-down trading near the end of the month.1 Equity returns in developed international markets were in line with those in the US, but emerging markets fared better than both. The US Federal Reserve, now under new leadership, continued holding interest rates steady amid an uptick in inflation. In the bond market, US Treasury prices fell as the benchmark 10-year yield rose to nearly 4.5%, close to its highest level in more than a year.2

The S&P 500 rose 10% and the tech-heavy Nasdaq added 14% as of June 19. Technology companies rebounded from an earlier decline by software stocks, as AI enthusiasm continued to boost chipmakers and others benefiting from spending on artificial intelligence. Shares of SpaceX made their debut in June in what was the largest IPO on record; it was among a handful of expected offerings from large technology firms this year, including several AI-related companies.3

Oil prices surged after the US and Israel struck Iran in late February, with hostilities continuing in the following months. A new ceasefire agreement was reached in mid-June.4 For investors, it is worth remembering that global equity returns have not been highly correlated with the level of oil prices. While the cost of oil may have some impact on stocks, it is just one of many factors to consider when looking at overall market performance. Furthermore, the US economy may be less impacted by oil shocks now than at some times in the past, as the economy has become more services-oriented and oil sources are more diversified.

Global equities, as measured by the MSCI All Country World Index (net dividends), rose 12% as of June 19. Stocks in developed international markets outside the US added 10%, as measured by the MSCI World ex USA Index (net dividends). The MSCI Emerging Markets Index (net dividends) fared much better, gaining 29%.5 Global equity markets have remained near record highs despite geopolitical conflict. This outcome is not surprising given how markets have fared in previous events. Looking at 21 of these over 36 years, returns were slightly negative for the first five days, but then turned positive over subsequent horizons. This would seem consistent with the market resetting prices in light of negative news at the start.

Likewise, results in 2026 haven’t helped support the common belief that precious metals such as gold hedge adverse conditions in the world. Since the onset of the war in Iran on February 28, an investment in gold has fallen by nearly 20%, erasing much of its strong gains from earlier in the year (see Exhibit 1). By comparison, the S&P 500 Index is up almost 10% over that same time period.

EXHIBIT 1

All That Glitters

Gold vs. S&P 500, total returns for 2026 as of June 19

Source: Dimensional Fund Advisors

This reinforces the importance of evaluating the role assets play in a portfolio. Stocks offer something in exchange for their risk: a positive expected return. In contrast, it’s challenging to support positive expected returns simply for holding gold. Note, too, that the precious metal has had negative years more frequently than the US stock market.

Inflation Persists

At its most recent meeting in June, the US Federal Reserve held the federal-funds target rate steady at 3.5% to 3.75%.6 It was the first meeting under new Fed Chairman Kevin Warsh. The decision came amid an increase in headline inflation, which rose to its highest level since 2023. Productivity growth, strong capital investment, and job gains also influenced the decision. Core inflation, which excludes more-volatile food and energy items, remained relatively steady in May, rising 2.9% from a year ago.7

Market expectations for a rate cut this year have been reduced, especially since the start of the war in Iran. According to CME Group’s FedWatch tool, the probability the fed-funds rate would be lower than the prevailing rate after the Fed’s December meeting was 96% in late February; the odds now favor a rate increase before the end of the year. This swing seems attributable to inflation concerns partly driven by rising oil prices stemming from the conflict in the Middle East.

In the bond market, US Treasuries fell 0.3%, sending the yield on the benchmark 10-year Treasury up to 4.46% as of June 19.8 The broader bond market was slightly higher, with the Bloomberg US Aggregate Bond Index up 0.02% and the Bloomberg Global Aggregate Bond Index (hedged to USD), a broad benchmark of sovereign and corporate debt, rising 0.7% as of June 19.9

Small and Value Start the Year Strong

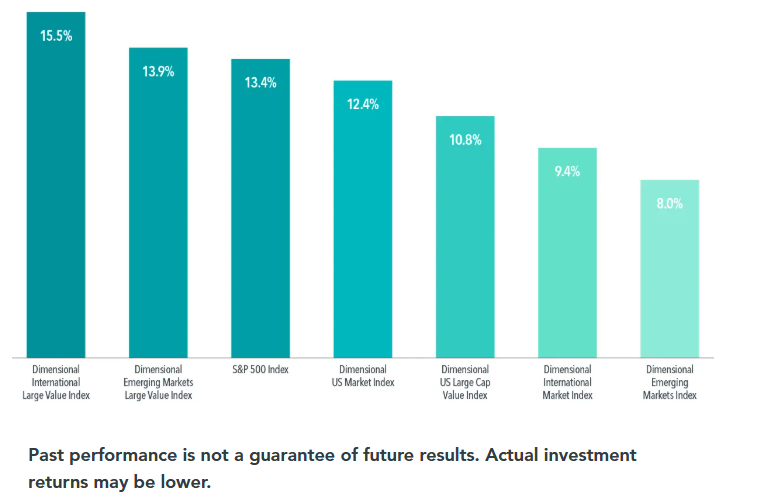

Small cap and value stocks, or those with low relative prices, had a strong first half of the year in the US, a notable shift from their underperformance in 2025. Large cap stocks with growth characteristics, or higher relative prices, were particular laggards in the US and globally.10 Over the past five years, non-US developed market value stocks have quietly led among equity asset classes (see Exhibit 2), which may surprise some investors. Elsewhere, high profitability stocks were outpaced by low profitability stocks in global developed markets, while the opposite was true in emerging markets.11

EXHIBIT 2

Leader of the Pack

Five-year returns for asset classes as of June 19, 2026

Source: Dimensional Fund Advisors

The first half of 2026 has only reinforced the broader point of Exhibit 2—that it’s difficult to predict which stocks, sectors, or regions will lead from one period to the next—with emerging markets outpacing developed markets and small value beating large growth. Rather than trying to guess the next winner, investors may be better served by maintaining exposure to equities around the world. Global diversification helps ensure that when leadership shifts across regions, as it often does, investors are positioned to participate in those gains.

- S&P data © 2026 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. Data as of June 19; Connor Smith, “S&P 500 and Nasdaq Tip-Toe Toward Fresh Records,” Barron’s, May 27, 2026.

- Returns are based on the Bloomberg US Treasury Bond Index as of June 19. Bloomberg data is provided by Bloomberg Finance LP. Source for US Treasuries: US Department of the Treasury.

- Corrie Driebusch, “SpaceX Officially Raises $75 Billion in Record-Breaking IPO,” The Wall Street Journal, June 11, 2026.

- Josh Dawsey, Anat Peled, and Benoit Faucon, “US and Iran Have Reached a Deal to Stop Fighting, Reopen Shipping,” The Wall Street Journal, June 14, 2026.

- MSCI data © MSCI 2026, all rights reserved. Data as of June 19.

- The federal-funds rate is the overnight interest rate at which one depository institution (like a bank) lends to another institution some of its funds that are held at the Federal Reserve. Source: “Federal Reserve Issues FOMC Statement,” Federal Reserve, June 17, 2026.

- Inflation data is as defined by the consumer price index from the US Bureau of Labor Statistics; the core CPI is an aggregate of prices paid by urban consumers for a typical basket of goods, excluding food and energy; Jed Graham, “Core CPI Inflation Eases Fed Fears as Warsh Takes Helm,” Investor’s Business Daily, June 10, 2026.

- “Daily Treasury Par Yield Curve Rates,” US Department of the Treasury. Data as of June 19.

- Bloomberg data provided by Bloomberg Finance LP.

- The MSCI All Country World Small Cap Index (net dividends) advanced 15.7%, while the larger cap MSCI All Country World Index (net dividends) rose 11.9%; The MSCI World Value Index (net dividends) gained 10.2%, while the MSCI World Growth Index (net dividends) rose 9.5% as of June 19. The Russell 3000 Value Index (net dividends) added 16.3%, while the Russell 3000 Growth Index rose 5.2%; the Russell 2000 Index (small caps) gained 20.7%, while the Russell 1000 Index (large caps) added 10.0%. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell indices.

- The Fama/French Developed High Profitability Index gained 6.5% versus an increase of 14.8% for its low profitability counterpart as of June 19; the Fama/French Emerging Markets High Profitability Index rose 35.4%, while its low profitability counterpart added 5.4% as of June 19. The Fama/French indices represent academic concepts that may be used in portfolio construction and are not available for direct investment or for use as a benchmark. Fama/French Developed High Profitability Index: Provided by Fama/French from Bloomberg data. Includes stocks in the upper 30% operating profitability (OP) range in each region; companies weighted by float-adjusted market cap. Rebalanced annually in June. OP for June of year t is annual revenues minus cost of goods sold; interest expense; and selling, general, and administrative expenses, divided by book equity for the last fiscal year-end in t – 1.